Recessions likely amidst global realignment

- 01 December 2022 (5 min read)

Key points

- We expect inflation to fall back towards target over the coming two years as global growth slows, with recessions forecast in both Europe and the US

- The Ukraine war and wider geopolitical tensions are causing a realignment of energy and wider supply chains tracking broad geopolitical contours

- Inflation looks set to fall but pressures on government finances have created social strains

- Structural changes from an ageing workforce and post-pandemic effects add to the uncertainties

Previous shocks continue to pose threats

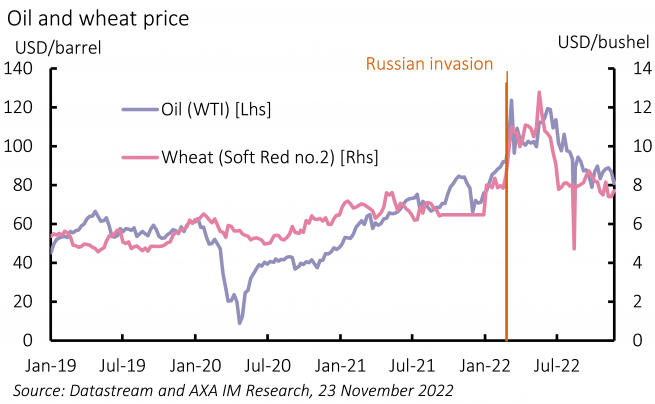

Our outlook and expectation for 2023 and 2024 is to finally see inflation retreat towards central bank targets against a backdrop of soft global growth, with recessions in Europe and the US, alongside a lacklustre recovery in China, before a slow recovery emerges in 2024. We recall that two of our last three Outlooks were rewritten within months of the new year. The first after COVID-19, which had not even been identified as we went to print; the second after Russia’s invasion of Ukraine, which added further impetus to inflation from disrupted energy and food markets (Exhibit 1). Chastened by both experiences, we cautiously consider the risks around this year’s Outlook.

The pandemic led to the wildest swings in GDP on record. The most obvious present threat from COVID-19 is in China. China’s initial success in containing the virus has been followed by slow preparation towards living with it. It recently announced measures to tackle this by accelerating vaccination rates and increasing medical capacities. But it is doing so against a renewed outbreak, which still threatens interim restrictions. The trade-off between loosening restrictions and increased vulnerability will persist and likely weigh on Chinese activity across 2023. However, COVID-19 remains a global risk as the threat of immunity evading mutations still exists – this is difficult to quantify risk, but we assume it is easing.

The war in Ukraine continues but recent Ukrainian successes in the East and South highlight the unpredictable nature of the conflict which some had thought Russia would quickly win. As Russia conscripts hundreds of thousands to the region, an end does not appear in sight. Moreover, there are risks that it could even escalate, either accidently or with Russia threatening the use of nuclear or chemical weapons.

Geopolitical risks are not restricted to Europe. Tensions between the US and China have worsened in recent years. Recent talks between Presidents Joe Biden and Xi Jinping offer hopes of arresting a further deterioration. Taiwan remains a key source of tension. The US has also imposed significant restrictions on the export of high-end technology to Chinese companies perceived as colluding with the military. In practice, this casts the net widely and with the US pushing for third-party enforcement, this could materially restrict Chinese access to semiconductor technology. This risks impacting China’s potential growth and it could also have a broader impact on global trade. Yet combined with a post-pandemic realignment of global supply chains, including a mix of on-shoring, near-shoring or friend-shoring, there is a marked uncertainty over the scale and impact of any deglobalisation.

A global realignment of energy supply is already underway, along the lines of broad geopolitical contours. Europe faces the end of cheap and plentiful natural gas supply, a constraint likely to drive it into sharp recession this winter. Without the swift installation of additional liquefied natural gas (LNG) import capacity, this will also impact next winter. LNG terminals are also being pushed to their limits, with US and European facilities run at materially higher load factors than before, with associated risks e.g., the explosion at the US Freeport terminal. Europe is also about to impose a ban on Russian oil, with the US to implement a price cap. Both risk uncertain reactions.

The outlook for energy markets also depends on the weather. A mild start to the Northern Hemisphere winter should help Europe. This is consistent with a La Niña weather system over the South-Eastern Pacific, which is entering its third year and often sees milder European winters. This will, however, also drive torrid weather conditions elsewhere. Moreover, climate change is driving trend temperatures higher but also increasing weather extremes. This will affect energy but will also have a profound impact on food production.

Inflation, government pressures and elections

Inflation has been the most obvious consequence of additional supply shocks. We expect inflation to ease from the start of 2023. Disinflation will vary from country to country, reflecting different economic conditions and local norms in terms of expectations and pass-through. Meanwhile, persistently high levels of inflation are having material societal impacts. In developed economies inflation is draining government finances, requiring public belt tightening, which can lead to social unrest. For emerging markets (EM), food and energy inflation have a more direct impact on overall price levels and historic periods of EM social turbulence have occurred during times of high inflation.

Governments face increasing strain over the coming years. EMs are impacted by tight global financial conditions, particularly an elevated dollar. Some ‘frontier’ economies have already fallen into financial crisis, with several appealing to the IMF. This will likely continue in 2023. Larger EM economies face the same risk, but we but do not see a systemic EM crisis evolving. Risks are not confined to EMs. The UK saw its fiscal sustainability questioned in 2022 and requires severe austerity over several years to restore fiscal rectitude. Many European states have a worse starting point and markets will monitor developments closely as the European Commission negotiates medium-term debt strategies with these countries.

The electoral timetable does not suggest significant political change over the coming years. We think Turkish elections in June 2023 could present further financial stability challenges. In developed markets, after Northern Ireland Assembly Elections expected in 2023, the UK faces a General Election in 2024. Current polls suggest a change of government, but with both parties having recently moved towards the political centre, this election promises to be the least economically damaging in over a decade. US Presidential Elections will be held in November 2024. Midterm elections further damaged former President Donald Trump’s standing, but he has still announced that he will stand for re-election. President Biden’s better midterm performance would help his cause, but it is not obvious that he will seek a second term. Uncertainty thus surrounds both parties’ nominees for the 2024 elections.

Forecasting uncertain amidst structural change

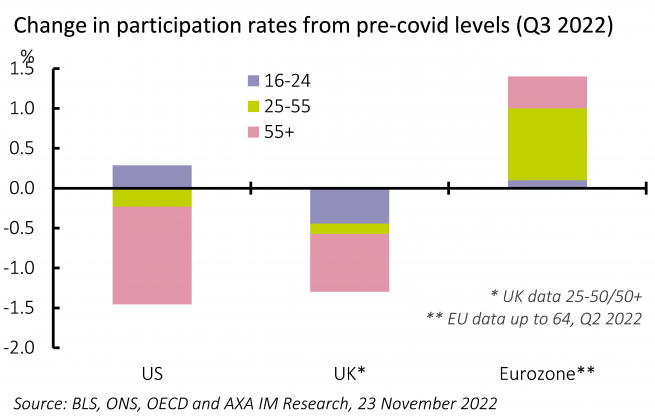

Most importantly, these developments take place amid ongoing structural changes, including shifting demographics – ageing in key economies – and post-pandemic reorganisation (Exhibit 2). We predict unemployment will rise across Europe and the US in 2023 but not as sharply as previous downturns. In part this reflects the particular tightness in the labour market and an expectation that falling vacancies, rather than job losses may do more to loosen the market. In part it reflects the withdrawal of labour supply as a result of both the pandemic and ageing. The combination has been a long-term headwind to potential growth which we expect to persist into 2023.

We expect recessions in Europe’s economies, driven by the energy shock. We also forecast a mild recession in the US –more a consequence of tighter financial conditions in response to excess inflation pressures. We expect China’s growth outlook to remain relatively subdued, forecasting another contraction in Q1 GDP as COVID-19 restrictions make an impact again. We forecast global growth of 2.3% in 2023, compared to IMF forecasts of 2.7%, and only expect 2.8% in 2024.

Central banks quickly tightened policy as inflation rose in 2022, but this poses risks for 2023. Forward-acting monetary policy tools employed using backward-looking data are a recipe for over-shooting. Some central banks appear to be shifting to a more forward-looking approach, led by the Bank of England (BoE), but with a noteworthy shift from the Federal Reserve. The onset of recession in many economies should soon mark the peak in interest rates although persistently resilient labour markets are an upside risk. Across Europe, we forecast peaks at lower rates than markets expect.

We are also cautious that inflation may take longer to moderate than markets consider, likely deferring future easing in the monetary stance to 2024 for most. In EM, Latin American countries quicker to tighten could begin easing later in 2023, including Brazil, Peru and Chile. In developed markets, the BoE may be among the first to ease, perhaps joined by the Bank of Canada if the housing market reverses more sharply than we expect. Rate policy may also be affected by balance sheet policy, all but relegated to background noise by many central banks, but we think it is likely to have more visible impact across the course of 2023.

Our views for 2023

Read our full outlook to find out more about our experts' views.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities. The strategies discussed in this document may not be available in your jurisdiction.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee that forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.