A wake up call for the energy sector? The IEA's path to net zero

- 21 June 2021 (7 min read)

The International Energy Agency’s 18 May report setting out one potential pathway to net zero makes clear the immense challenge ahead for energy companies and their investors.

The energy industry lies at the centre of any attempt to deliver on the goals of the Paris Agreement on climate change. Huge changes in production and consumption are required if the world is to reach net zero emissions and to minimise the global temperature increase to +1.5°C of pre-industrial times, so the International Energy Agency’s (IEA) 18 May report setting out one potential pathway is of great interest. It is a complex, detailed assessment of how the world might press ahead – and it makes clear the immense challenge ahead for energy companies and their investors.

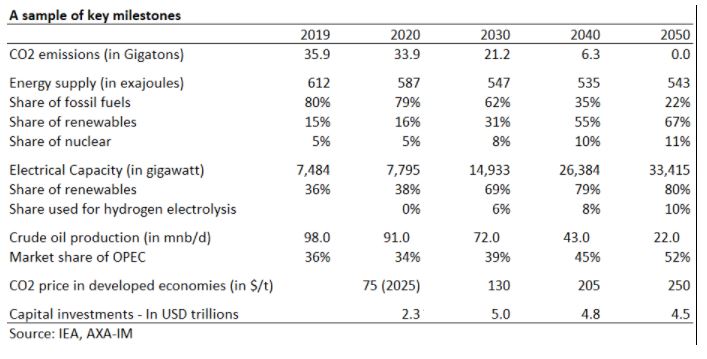

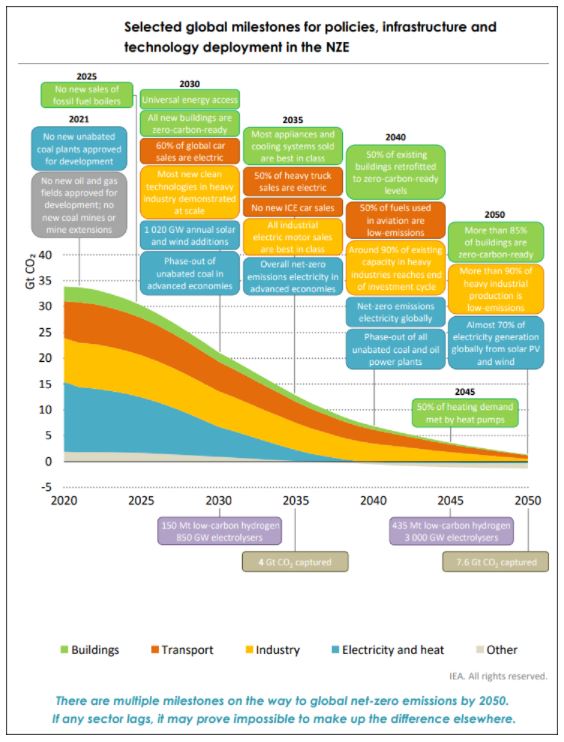

The report assumes that the desired outcomes of net zero and +1.5°C are indeed to be achieved by 2050 and then backtracks to 2020 to assess what should be done to succeed. This touches on supply and demand of energy, technologies, carbon pricing, social justice, the role of governments, and the role of investors. All the points are inter-related and interdependent. If some developments do not occur, more will have to be done elsewhere. Overall, the IEA has listed 400 milestones that underpin the trajectory to net zero.

Dr Fatih Birol, Executive Director of the IEA, insists that this is a path, not the path. It joins other assessments, such as that published by the Intergovernmental Panel on Climate Change in 2018 and should be assessed as a whole package, with individual conclusions not taken out of the broader context. It is not simply about oil and gas, but about the entire energy ecosystem. In our view, the most salient and striking points are as follows:

- Speed is of the essence and the transition needs to accelerate today, with significant progress required by 2030 to achieve the temperature objective

- It is as much about supply as it is about demand, with the steep decline in fossil fuels over the next decades being matched by the deployment of substitutive technologies

- It is mostly about developing more renewable energy (largely electricity), the electrification of whatever can be electrified, creating a hydrogen economy, pushing efficiencies to the fore and capturing emissions that cannot be abated

- It is global. Governments need to be involved, everyone will have to change many habits, it will require trillions of dollars of investment

- One of the IEA’s standout conclusions is that there should be no new developments of oil and gas fields from now on. This has generated perhaps the most heated debate, but curiously, an explicit call for a doubling of nuclear electricity capacity has gone down relatively smoothly

The IEA’s Net Zero Emissions by 2050 (NZE) scenario

Source: IEA. Note: ‘Low-emissions’ includes the use of fossil fuels with carbon capture, utilisation and storage (CCUS) and in non-energy uses

If the IEA’s scenario is to become a reality, we think it will first face many hurdles. As with every proposed pathway to net zero/+1.5°C it will require sustained, global political and societal support as well as the large-scale reallocation and deployment of capital. Beyond that, the IEA report makes clear how essential it is that everything is done in parallel, given multiple mutual dependencies.

For instance, a high cost of carbon is an absolute necessity to deploy many technologies; the growth of hydrogen is connected to the growth and declining cost of renewable electricity; the decline in gasoline demand is linked to the penetration of electric vehicles that itself is linked to the development of a charging infrastructure and further improvement in battery technologies.

Indeed, one of the crucial findings from the IEA is that some 46% of the technologies needed – in batteries and much else besides – are simply not yet ready and must be matured, industrialised, or even invented.

And perhaps the ultimate hurdle to clear lies in the tremendous ubiquity of fossil fuels. In the spring of 2020, when economies stalled as the COVID-19 pandemic raged, oil demand fell by “only” 25%. Even at what felt like a standstill for so many of us, the turbines were still whirring, the boilers still running, the emissions still escaping.

For AXA IM, and for all investors, the IEA report spotlights risks and opportunities. Many business models will be disrupted and may be rendered obsolete. Companies, even countries, will have to rethink their role in the energy ecosystem, and not all will come out healthy. Rules and laws will combine with social pressure to influence and oblige those entities to act. It is not, however, all doom and gloom. Opportunities abound already and more lie on the net zero pathway, be it in new clean technologies or new business models. Investors must carefully pick their way through this minefield if they are to deliver performance alongside sustainable climate solutions.

As investors wrestle with these era-defining issues, the IEA report has helped to illustrate the challenge of achieving this net zero/+1.5°C pathway. We can imagine the milestones as 400 walls, one laid out after the other and each one with a single door. We – investors, governments, and consumers – must line up those hundreds of doorways if we are to reach the prize on the other side.

In all likelihood, the IEA’s precise scenario will not come to pass. There are so many variables, and some of the milestones are more challenging to achieve than others. In our view, the goal of reducing oil consumption by more than 20% by 2030 will be tough, and the suggestion of building more nuclear capacity in the Western world will likely meet significant resistance. Other milestones, such as the development of renewable electricity, will build on existing momentum and have an easier route.

AXA IM has committed to reduce the carbon profile of its investment portfolios to net zero by 2050 or earlier. Although the IEA report will not on its own define our policy, its conclusions and the path outlined will be integrated in our analyses and contribute to our thinking. We expect many others to do likewise.

The picture will change. New trends and imperatives will emerge, but the levers and tools – and the challenges – of what it will take to reach net zero and keep temperatures in check are all accounted for in the IEA report. It has been called unrealistic or provocative and even a fantasy by some, but ambitious and feasible by others. Either way, it feels like a watershed moment, when the industry at the heart of the problem snapped to attention – that alone should help build momentum towards net zero.

Ultimately, the IEA has set out a demanding scenario, and highlights with great clarity how dramatic and disruptive the energy transition will be. It shows that social, financial and political capital needs to be harnessed today and for decades to come. There is much to consider for investors here, perhaps most notably the call for an end to new oil and gas fields, but through every one of those 400 milestones lies a fresh challenge for all stakeholders – and for all our ways of life.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.