US equities - Artificial intelligence: Not a bubble… yet

Artificial intelligence (AI) is the most impactful digital transformation theme since the development of the Internet. The public launch of ChatGPT in November 2022 catalysed a wave of investment and innovation that continues to build momentum. As excitement about the potential for this new technology builds toward very high expectations, investors and industry participants are questioning if we are entering a bubble. Our current conclusion is that AI is not a bubble… yet. We are carefully monitoring risks and similarities to the Internet and telecom bubble (the “dotcom era”).

Risks and similarities include:

- The desire to be first to market with leading AI models is creating an arms race that may result in an overbuilding of infrastructure, as not all players will be successful.

- Massive up-front investment is required for training and running AI models, with revenues and earnings expected at some future date. This creates uncertainty about the return on invested capital (ROIC) for many AI initiatives.

- The emergence of debt financing including the use of private credit and off-balance sheet structures (joint ventures and special purpose vehicles), and the reported use of Graphics Processing Units (or GPUs, these are fast-depreciating assets) as collateral in some cases, introduces significant risk.

- The existence of circular relationships among suppliers and customers is a red flag. We are concerned about the systemic risk associated with the interrelated financial dependencies.

On the positive side, there are several mitigating factors that make us confident we are not yet in bubble territory.

The leading cloud service providers (CSPs) are large, rational companies with strong balance sheets and positive free cash flow generation. To date, they have self-funded their AI capex primarily through operating cash flows. During the Internet and telecom bubble of the late 1990s, the companies bearing the brunt of the infrastructure investment were primarily debt-funded and did not have stable cash-generating business segments to support them through the cycle.

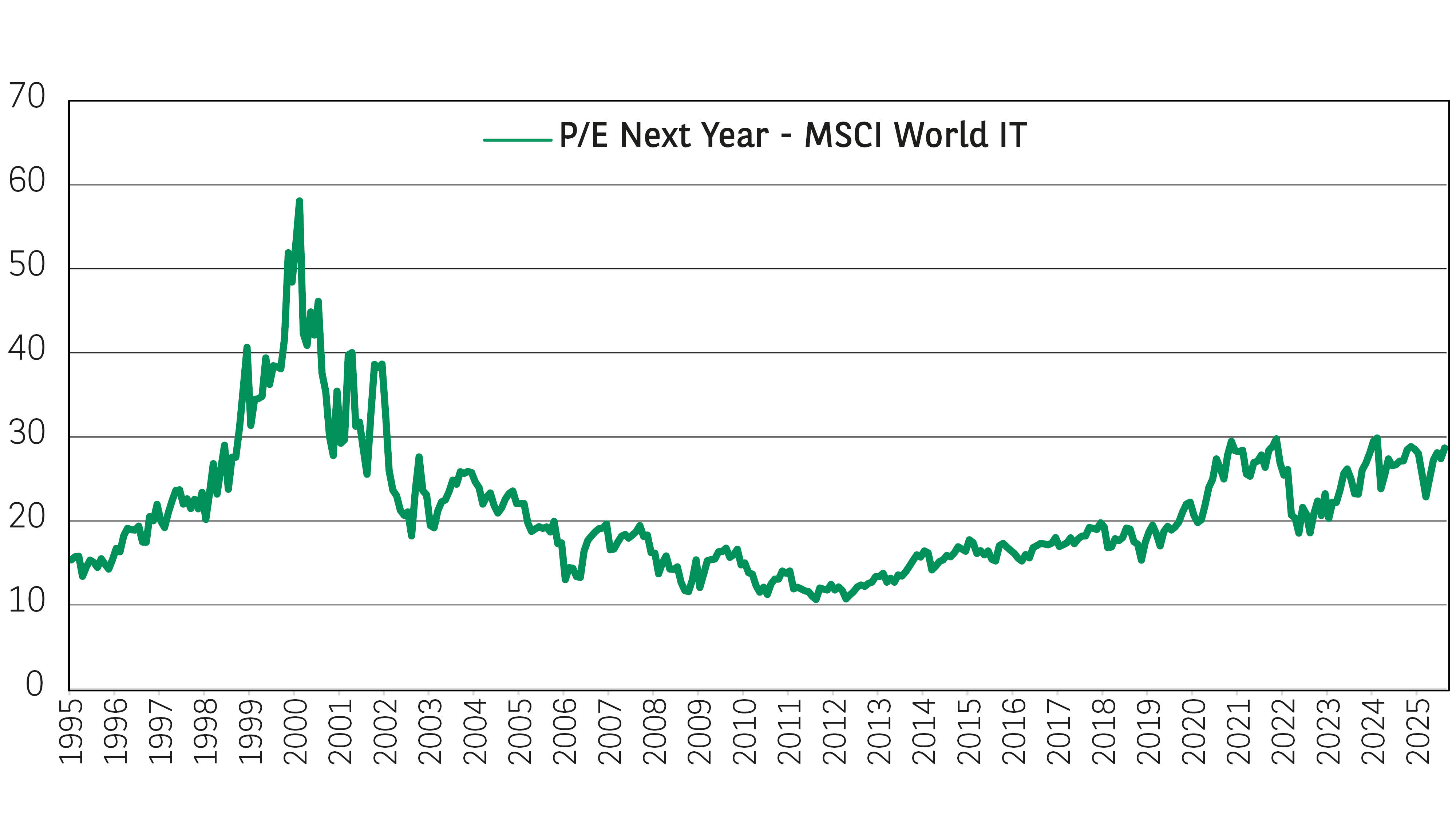

Exhibit 1: Valuations of the MSCI World Information Technology (IT) Index are far from dotcom bubble levels

Data as at 30 September 2025. Source: MSCI, Bloomberg

It is still very early in terms of the adoption of AI, and potential use cases are expanding. A recent survey found that while 78% of enterprises are using AI in at least one department, only 16% have deployed it across five or more1. Agentic AI holds the promise of enabling new use cases where autonomous agents, powered by AI, will reason, plan, and act across IT systems and data, and thus automate many tasks. Physical AI is also on the horizon as AI converges with robotics and other consumer devices. In technology adoption cycles, it is not unusual for steep investments to occur ahead of widespread monetisation.

The infrastructure exists (in the form of high-speed Internet access, smartphones, and other connected devices) to immediately deliver AI-based applications to end users. That was not true during the Internet and telecom bubble, as the fibre buildout occurred well ahead of the existence of the “last mile” networks that provide broadband access, and well before the availability of smartphones. This enables innovators to achieve faster time to revenues and returns. For example, ChatGPT has already reached 800 million weekly active users in less than three years, as of October 2025, compared to 13 years for Internet adoption.

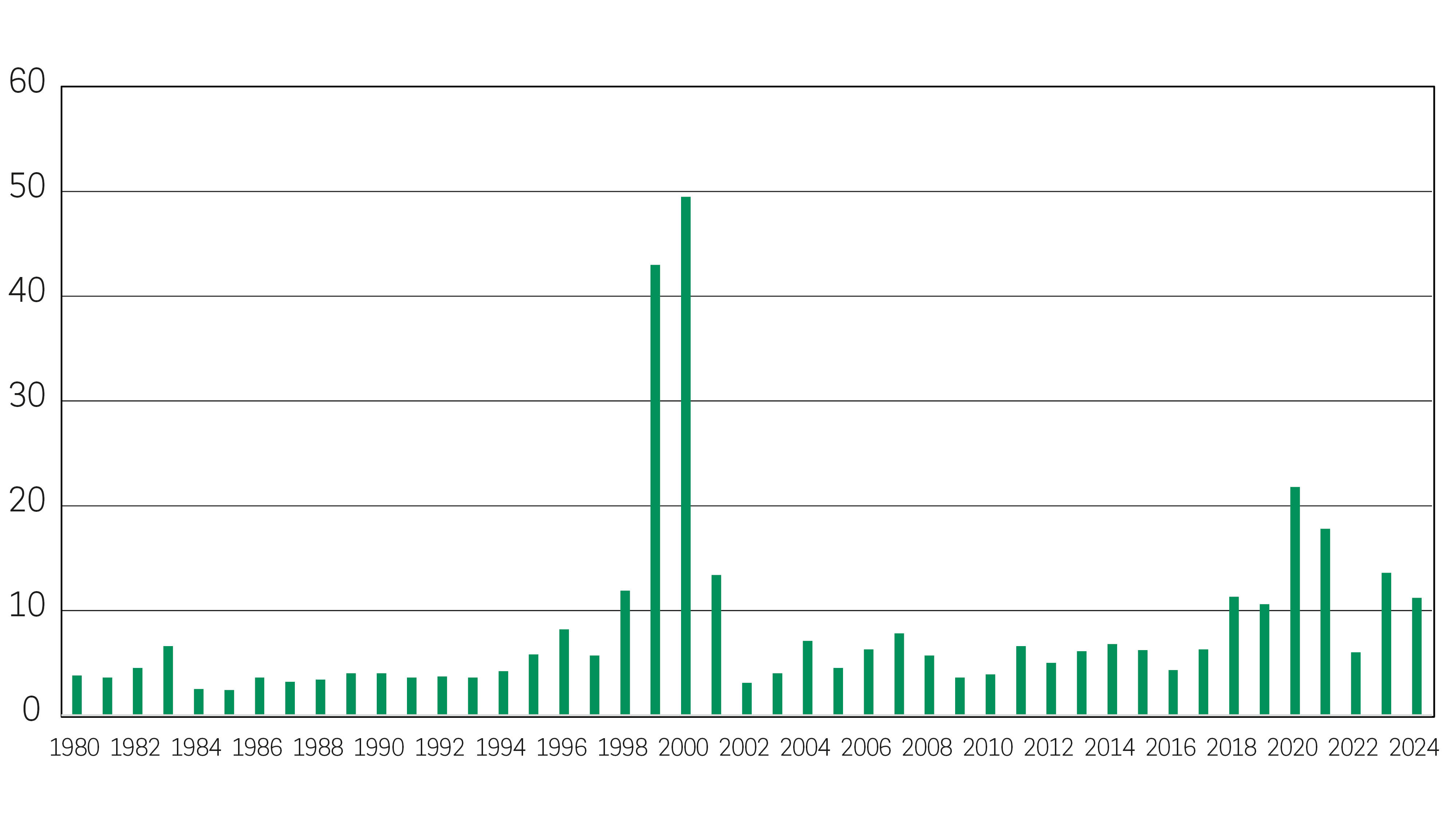

Exhibit 2: Tech sector Initial Public Offerings (IPOs), median price/sales multiple by year

Data as at 29 September 2025. Source: Initial Public Offerings: Updated Statistics, Jay R. Ritter, University of Florida, table 4a.

Valuations of publicly traded technology stocks are not nearly as stretched as in the late 1990s. While expectations are high now as they were then, the valuations are still reasonable for many leaders in AI. In a bubble, valuations become untethered from reality, with investors paying high multiples on heightened forecasts. We believe some of the more speculative valuations in AI today are concentrated in the private markets, with most AI companies staying private for longer, thus insulating the public equity market.

- Source: McKinsey & Company, March 2025. The state of AI: How organizations are rewiring to capture value

Today we have reasonable multiples on high expectations. Higher multiples compared to 10 years ago reflect higher profit margins and returns on equity (ROE) of growth companies.

During the Internet/ telecom bubble, high multiples were placed on high expectations. For example, the median price to sales multiples of tech sector initial public offerings (IPOs) spiked to 43x in 1999 and 49.5x in 2000.

In conclusion, we believe the AI theme is not yet in bubble territory. Expectations for the leaders of AI are high, but valuations remain reasonable. However, we are aware of and monitoring several risk factors going forward and are watching for signs of a digestion period in the spending cycle. It is possible that industry consolidation and disruption will occur over time as winners emerge from the arms race. We remain intensely focused on bottom-up fundamental research at the company level to identify winners and avoid losers, and on monitoring developments closely as the adoption of AI progresses.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.