EM reaction: a surprise 500bp rate hike in Turkey in March, month of local elections

KEY POINTS

A bold rate hike in March and renewed commitment to tame inflationary pressures

The Central Bank of Turkey (TCMB) hiked their policy interest rate by another 500bp at its March monetary policy meeting, which were at odds with Bloomberg’s consensus expectations of the Bank staying on hold.

The more recent slippage of inflation expectations has indeed further pressured the lira, opening the door for more action from the central bank. Its decision to tighten its macroprudential framework yet again by reducing loan growth limits, three weeks ahead of today’s meeting (on March 1st) had raised doubts about possible political constrains around the central bank upon its ability to deliver further rate hikes, particularly in the context of local elections taking place at the end of the month. This was proven wrong by today’s bold move, the first hike under the new Governor Mr. Fatih Kharan who took over in January after Ms. Erkan’s resignation. Furthermore, the official statement continued to retain a hawkish forward guidance: “Tight monetary stance will be maintained until a significant and sustained decline in the underlying trend of monthly inflation is observed, and inflation expectations converge to the projected forecast range. Monetary policy stance will be tightened in case a significant and persistent deterioration in inflation is foreseen.”

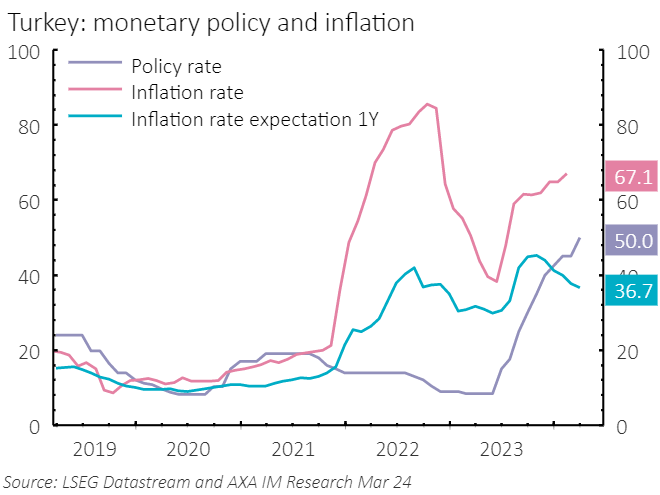

Interest rates have been hiked by a cumulative 4,150bp from 8.5% in May 2023 to 50% in March 2024, as the economic team following the re-election of incumbent President Recep Tayyip Erdoğan was given the mandate to tackle the various imbalances accumulated by the Turkish economy these past years. The most pressing ones included an overheated credit-fueled economy; excessively high inflation and de-anchoring of inflation expectations; massive external financing needs; insufficient reserves at the central bank; significant slippage of public finances and accumulating contingent liabilities. Ten months since the last general elections (May 2023) and just a few days away from local elections (31 March), many of these issues remain, some have worsened. 2023 GDP growth recorded at a staggering 4.5% (4% year-on-year in Q4), but more importantly, the third year of a double-digit contribution from domestic demand, signaling obvious overheating. Monetary policy has become more orthodox, and today’s bold move further improved the credibility of the central bank. Currently, we project inflation to accelerate to above 70% by mid-year and decelerate towards 45% by year-end. At 50%, ex-ante real policy rates compensate for the continuous de-anchoring of inflation expectations and could be a sufficient tight stance to see disinflation taking place in H2 upon a tighter fiscal policy, but we acknowledge that there is a risk of seeing further monetary tightening if inflation pressures fail to decompress as fast as projected.

The inflation outlook remains bleak at the start of 2024, but we still expect disinflation to take place in H2 2024.

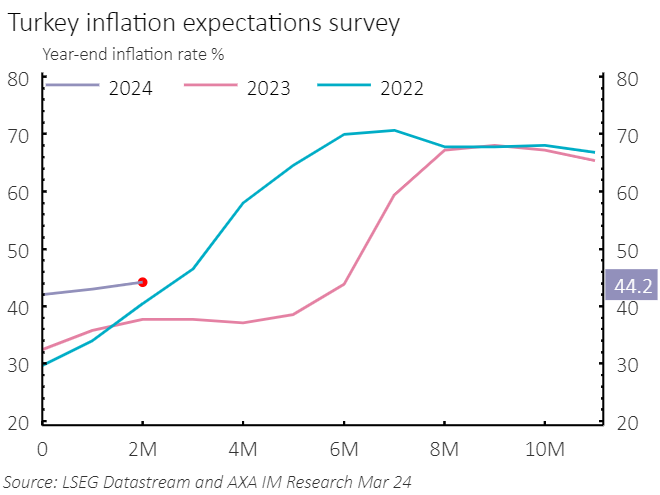

Inflation rate reached 67.1% year-over-year in February 2024 (72.9% for core inflation), more than double since June 2023 when it reached 32.8%. Services prices, in particular, which usually display more stickiness, have posted strong increases, annual inflation in the services sector accelerated further to 94.4%. On the goods side, the recent acceleration in FX depreciation points to deterioration in goods inflation which printed 57% year-over-year in February. Meanwhile, inflation expectations drifted further away from CBRT’s year-end forecast of 36%, with March survey pointing to year-end inflation rate projected at 44.2% up from 40% back in January. Projecting inflation ahead remains a very difficult task; as a theoretical exercise, if we were to apply as of March 2024 the average monthly inflation increases of the past four years, inflation rate would end the year at 49%. We assume a slightly slower pace of inflation as of mid-year on the back of a tighter policy mix (particularly the fiscal stance post-elections) that would dampen domestic demand into H2 2024, bringing the year-end inflation closer to 45% year-over-year.

Local elections (31 March) a few days away...

After having won Presidential and legislative elections back in May 2023, President Erdoğan’s AKP party is hoping to reclaim several major cities’ mayor positions, most importantly Istanbul, lost in 2019, Turkey's commercial hub of 16 million people (20% of the population). Undoubtedly, the AKP has a strong position into these polls. There is an obvious preference for dollar denominated assets ahead of elections in Turkey, and it needs to be seen whether this recent hike and the outcome itself of the ballot will achieve to balance the preference towards lira denominated assets in the next weeks/months. To this respect, President Erdoğan’s recent comments acknowledging that these local elections will be his “final” election seek to alleviate worries that he may call for yet another referendum in order to change the Constitution and grant him more time at the helm of the country. Rendez-vous on March 31st …

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© AXA Investment Managers 2024. All rights reserved

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.