How cost-conscious buy and maintain strategies seek to avoid pitfalls in credit investment

Key points:

- Buy and maintain strategies seek to outperform through fundamental credit selection, risk-optimised portfolio construction and minimising performance erosion from turnover.

- Reducing the impact of downgrades and refreshing the allocations from bond proceeds, client flows and limited turnover, builds resilience against changing market environments.

- By focusing on long-term credit fundamentals, buy and maintain strategies aim to avoid risky short-term exposures and instead provide stable returns and downside risk protection.

Bruno Bamberger, AXA IM Core Solutions Strategist

Buy and maintain (B&M) strategies can have the same characteristics and potential benefits of traditional credit portfolios. They can provide the yield, spread over government bonds, income and potential returns from the bonds held, as well as the potential to fulfil investors responsible investment objectives.

B&M credit strategies gained prominence with investors after the 2008 financial crisis. Investors were looking for relatively low-cost access to credit and baulked at the direct (fees) and indirect (trading) cost of fully active strategies, while seeking to avoid the inherent pitfalls of traditional passive strategies, such as being forced sellers of downgraded bonds or exposure to drifting risk profiles.

It offers advantages to different types of investor:

Multi-asset investors - exposure to credit more generally can, in our view, provide a clear de-risked and diversified option against risky assets, particularly now that government bond yields are significantly higher. Additionally, B&M risk exposures are designed to be relatively consistent throughout a market cycle, making it easier to understand and model risk exposure when allocating to credit.

Liability - and cashflow-focused investors – while the potential capital growth is a plus, interest-rate exposure and predictable income can be helpful for matching liability risks and cashflow requirements, for example for defined benefit pension funds and insurance companies.

Investors under accounting or solvency constraints – the low turnover and stable risk profile of B&M credit helps control profit and loss statements and maintain a constant solvency capital ratio.

Traditional passive investing in mutual funds is costlier than you think

In our experience, many new B&M investors already understand the inefficiencies and risks arising from traditional passive management. These can be split into:

1. index constituents – what names are included or removed from the index

2. index construction – the weight of names included in the index

1) Index constituents – the cost of downgrades and dropouts

Traditional passive strategies are bound by the composition rules of their index and will crystallise losses from forced sales from downgrades and those falling out of the index.

Most passive strategies are forced to sell bonds that have their credit rating downgraded outside of the parameters of the index they are tracking. For example, they will be forced to sell bonds downgraded to high yield in a passive investment grade fund. This is one of the largest indirect costs that passive investors will face and can outweigh the impact of lower fees between active (including B&M) and passive strategies.

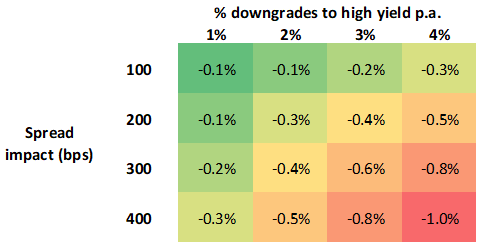

The table below shows the impact of a range of downgrade rate and spread impact scenarios on passive investors in mutual funds

Illustrative cost to passive investors for different downgrade and spread impact scenarios

Source: AXA IM, 31.05.2023

For context, as at 31 May 2023, the spread differential between the lowest broad rating bucket in investment grade (BBB), with the highest broad rating bucket in high yield debt (BB) was 176 basis points (bp), marginally above the 10-year historical average of 156bp.

Using this figure and taking the historical average level of downgrades to high yield (around 2% each year), the performance impact to traditional passive investors could be 20-30bp per year – materially higher than the ‘low fee’ that passive index tracking funds offer.

This risk is magnified during periods of economic stress, when both the level of downgrades and the spread impact could increase, as could the direct trading costs of selling those bonds. There should be no surprises here – market selloffs impact lower-rated bonds more than higher-rated bonds.

One final concern relating to index constituents is that bonds with less than one year of maturity are removed from the index (and therefore the passive strategies tracking those indices). Although the spread impact and trading costs of this are not significant, the systematic nature takes no regard of the timing of the sale from a relative value perspective.

2) Index construction – risk and responsible investment exposures

Passive strategies managed against traditional or ‘parent’ credit indices are bound by the construction rules of their index. Investors can face changing and unintended risk exposures while the pure replication aspect creates difficulties in being able to credibly integrate responsible investment into their investment process.

Allocations within traditional bond indices are typically weighted by the market value of their debt outstanding. Therefore, any issuer, country or industry that issues more debt will have a higher weight within the index, meaning that the most indebted and often most leveraged issuers may have greater weight within passive portfolios. This factor of index construction runs counter to the objectives of most investors when investing in bonds – i.e., stable capital growth and downside risk protection.

One example of this is the growth of the financial services sector before the 2008 financial crisis. The proportion of financials within the global credit index rose from 40% at the turn of the century to over 50% just before the crisis, due to the excessive lending and spending undertaken.

Investors may be unaware of the drift in risk characteristics of indices over time. As another example, the size of the BBB rated bucket has increased from 25% immediately after the financial crisis to 47% as at 31 May 2023, with the size of the very lowest rated investment grade category, BBB minus bonds, doubling in size to 10% over the same period.

Continuing the theme of risk management, many strategies may struggle to accurately integrate emerging concerns around responsible investment within a rules-based approach to portfolio construction, even a small amount of tracking error against a parent index can significantly improve a portfolio's responsible investment footprint.

While climate-related data has improved rapidly over the past few years there are still considerable improvements to be made, ranging from the accuracy and scope of emissions data, climate risk exposures and measurements of alignment to net zero. And the availability of data for biodiversity is still in its infancy – traditional passive strategies have no credible way to integrate these rapidly evolving measures into portfolios.

B&M has the potential to overcome both constituent and construction inefficiencies

B&M strategies are designed expressly to address these inefficiencies of traditional passive investing. They use careful downgrade management and an active investment process to deliver a flexible, risk-optimised portfolio, tailored to clients’ ongoing needs.

A B&M strategy has three routes to potentially minimise the negative impact from downgraded bonds:

1) Avoid bonds that will be downgraded in the first place – through the deep fundamental bond research and credit selection process of buy and maintain.

2) Mitigate risk exposures through active portfolio construction - while not all downgrades to high yield can be avoided, examples of mitigation include only holding lower credit quality bonds at shorter maturities or by holding broadly equal weighting to each bond to avoid an overconcentration of risk in a given name or sector.

3) Not blindly selling downgraded bonds – even when there is a downgrade to high yield, holding a bond provides the opportunity to outperform the index as bonds can recover over a fairly short time horizon.

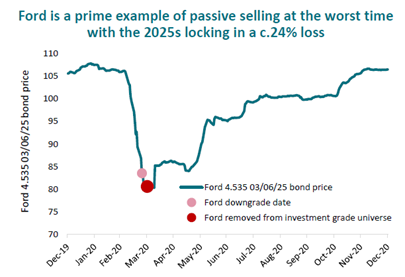

For example, Ford Motors, was downgraded in February 2020; holders of the 2025 maturity bond would have locked in a loss of around 24% if they had sold at the month-end following the downgrade date. But if they held on for another 3-6 months after that date they would have recouped most of that loss as the chart of the bond’s price below shows.

Source: Bloomberg, AXA IM, 31.05.2023

Some bonds are also downgraded for ‘technical’ reasons. This can happen, for example, if one of the three major rating agencies ceases to rate the bond or if leverage temporarily rises due to an acquisition – even if the fundamental profile of the issuer has not changed. In this circumstance, and other similar situations where our credit research team remains comfortable with the name, we could continue to hold the bond until maturity or until it is upgraded to investment grade again.

The same holds for bonds that have dropped out of the index due to being within one year of their maturity date, as mentioned earlier. Simply by holding the bond for an additional year or waiting until an appropriate moment to sell, can allow active investors to recycle the full proceeds into the next opportunity.

Not leaving responsible investing to chance

With regards to responsible investment, B&M strategies select bonds using a fundamental credit research process based on forward-looking and sector-specific risk characteristics and seek to overcome the nuances of working with incomplete datasets. This responsible investment integration complements, rather than counteracts, the financial objectives of a fund or portfolio.

The longer holding period of bonds in a buy and maintain portfolio neatly aligns with the timeframe over which climate, biodiversity and social factors need to improve. This arguably makes B&M one of the only fixed income strategies that can provide active and consistent funding to drive sustainability improvements in the underlying issuers.

To take the example of company-level engagement, investors can have a greater impact with issuers knowing that the portfolio manager can cease to re-invest in a name or even divest should engagement escalation not be successful. Passive funds will not have the flexibility to do that while other strategies may not have a long-enough holding period to see through required responsible investment improvements.

Finally, the responsible investment objectives of the fund/portfolio can be enhanced over time to reflect the latest and best practices in the market and include emerging themes such as social and biodiversity factors.

Can you be active in B&M strategies?

One of the arguments against buy and maintain is that it isn’t truly ‘active’. We disagree.

There are numerous levers B&M portfolio managers can pull to re-adjust portfolios and take advantage of prevailing market conditions. We purposely named our strategy ‘Buy and Maintain’ rather than ‘Buy and Hold’, to reflect the fact that we continuously look for new opportunities across markets. We’re willing to trade to try to enhance risk-adjusted returns if we believe those issuers are ‘money good’ and could be held to maturity.

First, any flows of cash into or out of the fund or segregated portfolio can be used to re-align the risk exposures, provide some yield enhancement, and help to achieve any responsible investment objectives. Many clients choose to top up their B&M portfolios when market yields or spreads are wide relative to historical levels or when dispersion appears across markets. Recent examples include the COVID-19 crisis (when dollar-denominated bonds were cheaper than peers) or the UK crisis around liability driven investment (LDI) when sterling bonds were cheaper.

Credit portfolios also benefit from natural cash injections by receiving the proceeds from bond coupons and maturities. For a typical global credit portfolio this amount can be 5-10% per year, enough to take advantage of the new issuance market premiums and to direct into attractive sectors, currencies, or issuers in a cost-effective manner.

Our B&M strategies are willing and able to undertake a moderate amount of active turnover, unless client guidelines advise otherwise. This turnover could be due to concerns about the fundamental viability of an issuer, for responsible investment concerns, or simply to improve the risk-adjusted returns of the portfolio.

Buy and maintain strategies would not, however, take significant active risk positions or pursue short-term tactical plays. We always target issuers with the intention of holding those bonds to maturity. This approach is designed to deliver more stable returns over a market cycle, while alpha is likely to be generated from credit selection, downgrade avoidance and smaller relative value plays rather than from running a high beta approach, which may underperform when markets sell off.

Knowing that the outright and relative risk exposures acquired at the outset are likely to remain consistent throughout the life of the portfolio can have numerous advantages. It can be helpful for multi-asset investors looking to build truly diversified portfolios and for institutional investors looking to maintain certain funding or solvency ratios.

Having a lower level of turnover and typically lower fees compared to other active strategies may also reduce the erosion of performance of credit portfolios over time, particularly in times of elevated uncertainly, which can raise trading costs.

Summary

Traditional passive strategies are bound by the index constituent and construction rules which can lead to significant drawbacks for investors. These include being forced sellers of downgraded bonds, shifting risk exposures to the most indebted sectors and issuers and the inability to integrate responsible investment within the investment process.

We think that through a pragmatic approach to managing downgrades that mitigates and monitoring risk levels through careful bond selection, buy and maintain investors can dodge these pitfalls in passive credit investing against traditional credit indices, while gaining relatively low-cost access to some of the key advantages of active management

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.