India - a bright spot in emerging markets

Key points:

- India’s gradualist approach to reform is providing the basis for sustained growth.

- The economy is now the fifth-largest globally and on track to become third-largest by the mid-2020s.

- We see the US dollar bond market as an easy way to gain exposure to India

India’s gradualist approach to reform has borne fruit over the past decade, contributing to an easing of fiscal constraints while providing the basis for sustained growth. A prime example of positive reform is the rollout of the Goods and Services Tax in 2017, which has widened the tax base and simplified the tax structure. The reduction in the corporate tax rate, meanwhile, from 30% to 22% in 2019

Other measures adding to this sense of change include:

- Changes to bankruptcy law since 2016

- The start of labour market reform, with the amalgamation of 29 different labour laws into four codes

- The creation of land banks through land acquisition by public bodies which has made it easier to acquire land for large projects

- Financial sector reforms

- Increased digitization that is improving administration efficiency.

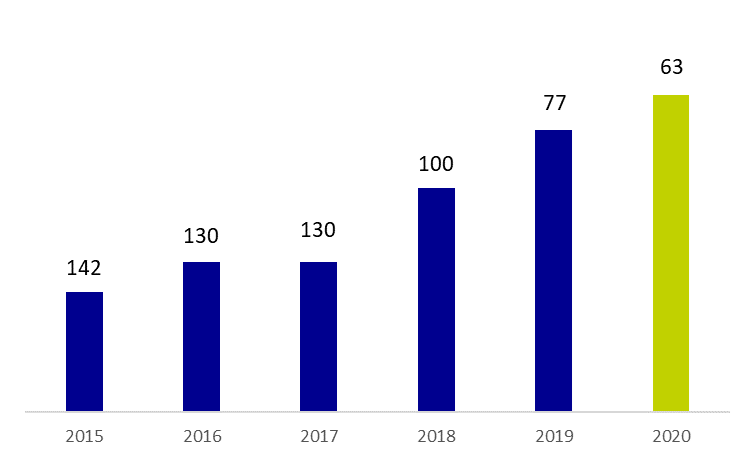

These have all contributed to a fall in the cost of doing business in India (see Figure 1).

Figure 1: India’s Ease of doing business ranking has improved

Source: World Bank, UBS, September 2023

Concurrently, there has been a massive overhaul of infrastructure in the country that has improved productivity and reduced logistical barriers. Examples include:

- National highways have doubled

- Renewable power generation has quadrupled

Source: Government of India - Railway electricifcation has seen a seven-fold increase

Source: Government of India - Upgrade of public digital infrastructure upgraded

In 2020, India launched the Production Linked Incentive Scheme, offering tax benefits for increased production across 14 sectors. This has helped to put India at the forefront of destinations for international firms to relocate out of China.

On track to be one of the world's biggest economies

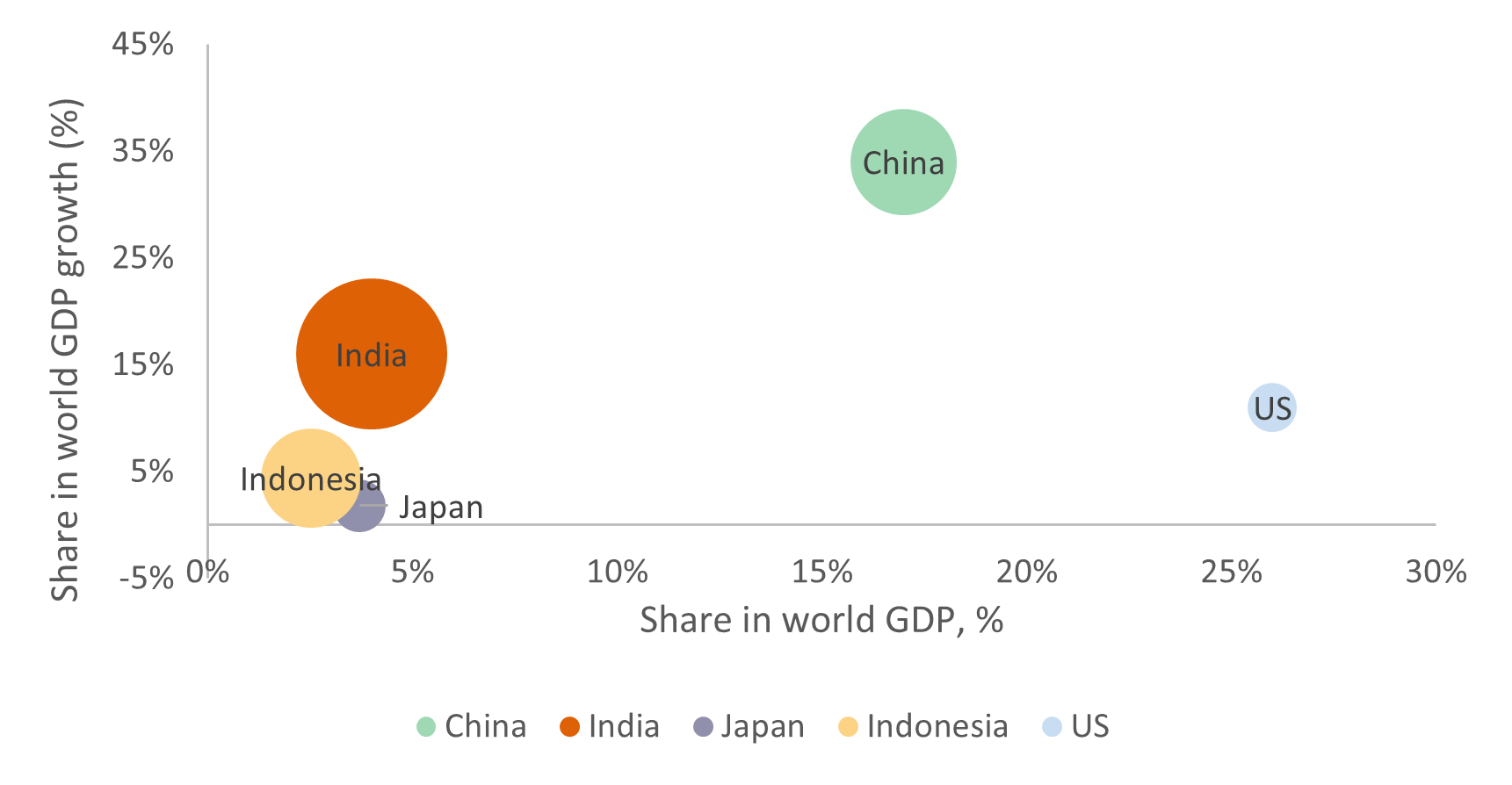

Results have begun to show. The Indian economy is now the fifth-largest in the world, and on track to become the third-largest by the middle of the 2020s. Foreign direct investment inflows have accelerated sharply to be consistently above $40bn annually from 2015-2022

Figure 2: Contributors to world growth in 2023 (estimated)

Source: AXA IM, IMF, UBS estimates, September 2023

Macro stability has been instrumental in that success. Gradual medium-term fiscal consolidation has allowed the Reserve Bank of India (RBI) to strike a balance between growth support and inflation control, with monetary tightening required by its inflation target more contained than in previous cycles.

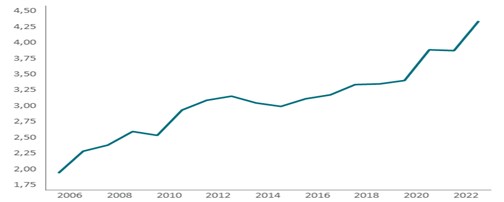

The largest improvement has been on the external front, also contributing to macro stability. India’s share in global services exports (approximately 5%) has more than doubled over the past 15 years and that of goods exports (approximately 1.9%) has also shown progress (see Figure 3).

Figure 3: Global share of India’s service exports (%)

Source: Macrobond, AXA IM – Real Assets, data as at September 2023

The service balance shows a sizeable structural surplus, which limits the sensitivity of the current account balance to faster domestic demand or higher oil prices. More recently, India has been protected from the impact of the war in Ukraine by its access to discounted Russian oil. The current account deficit has narrowed to a sustainable range of 1% to 2.5% of GDP

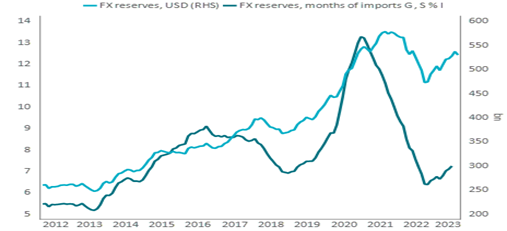

The RBI has built a war chest of foreign currency reserves ($530bn, seven months of total imports), allowing it to smooth excessive currency volatility.

Figure 4: Foreign currency reserves

Source: Macrobond, AXA IM – Real Assets, data as at September 2023

Improving access to international financial markets

International borrowing has been kept in check and external debt metrics compare favorably with India’s credit peers. The upcoming inclusion of Indian local currency government bonds in the JP Morgan GBI EM index marks another milestone in India’s journey to deeper financial markets and increased access to international savings.

Figure 5: External debt as a % of exports goods, services and income

Source: Macrobond, AXA IM – Real Assets, data as at September 2023

The dollar bond market provides a straightforward way to gain exposure to India, as there is a broad range of companies and public sector entities that have dollar bonds outstanding. Approximately 100 issuers from the country have issued US dollar bonds with a total outstanding of around $150bn

Within that opportunity set, we believe that companies operating in the renewable energy sector best fit our commitment to responsible investing and we hold these across portfolios. Looking at performance, the country subindex in the JP Morgan Emerging Market Corporate subindex outperformed the broad benchmark year-to-date (3.4% versus 2.1%

Overall, we believe India is a bright spot in emerging markets globally and the country represents a core holding across our portfolios.

Disclaimer

Not for Retail distribution: This marketing communication is intended exclusively for Professional, Institutional or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.