US Outlook – Avoiding recession leaves little space for easing

Key points

- The US looks set to slow but avoid recession. We see growth of 2.3% in 2023, 1.1% in 2024 and 1.6% in 2025. There are risks of a sharper slowing in H1 2024, before a pick-up in 2025

- Inflation should fall back to target in 2025 aided by labour market easing and structural improvement

- The Fed is likely to manage restrictiveness, rather than ease outright with QT likely through 2025

Phantom recession?

This time last year we forecast a mild recession in 2023. In fact, this year now looks on track for above-trend growth of 2.3%, thanks to a more resilient consumer, buffered by excess savings and solid hiring by a corporate sector which has avoided the worst excesses of Federal Reserve (Fed) tightening. A quicker pick-up in investment in response to government programmes also helped. The key question is whether recession has been averted or merely delayed. However, despite stronger growth, inflation fell quicker than we expected and is likely to average 4.2% in 2023 (5.1% expected) and Fed policy appears likely to peak at 5.25-50% this year – 50bps higher than forecast.

Growth below potential but should avoid recession

Despite a strong Q3 GDP expansion of 4.9% (saar) with consumer growth of 4.0%, we continue to expect a marked moderation in consumer spending to deliver a significant slowdown next year. We expect real disposable income to fall, with employment income growth softening quicker than inflation is easing, with an increase in tax contributions impacting disposable income growth. We are also wary that support from unwinding excess savings has run its course. The saving rate was estimated at 3.4% in September and we expect this to rise over the coming quarters.

We forecast a deceleration in consumer spending from Q4 that is likely to last through the first half of 2024 before improving. Risks surround this outlook; the treatment of excess saving is uncertain. We argue that late-summer spending suggested an income divide, with iPhone and auto sales offset by subdued clothing and food sales. Higher income households’ spending may remain supported by savings, even as buffers for lower income households appear exhausted. Households may also offset real income pressure by increasing borrowing – the sector is in a better position than 15 years ago.

Investment spending is also likely to slow but remain solid – we were surprised at how quickly it responded to policy stimuli. While this looks set to support spending in the immediate quarters, deceleration is likely for the coming year. However, without forecasting a major cyclical event, and with large businesses managing their financing to avoid a refinancing wall over the coming years, we expect investment to remain solid in the face of continued domestic demand, additionally underpinned by energy and artificial intelligence investment.

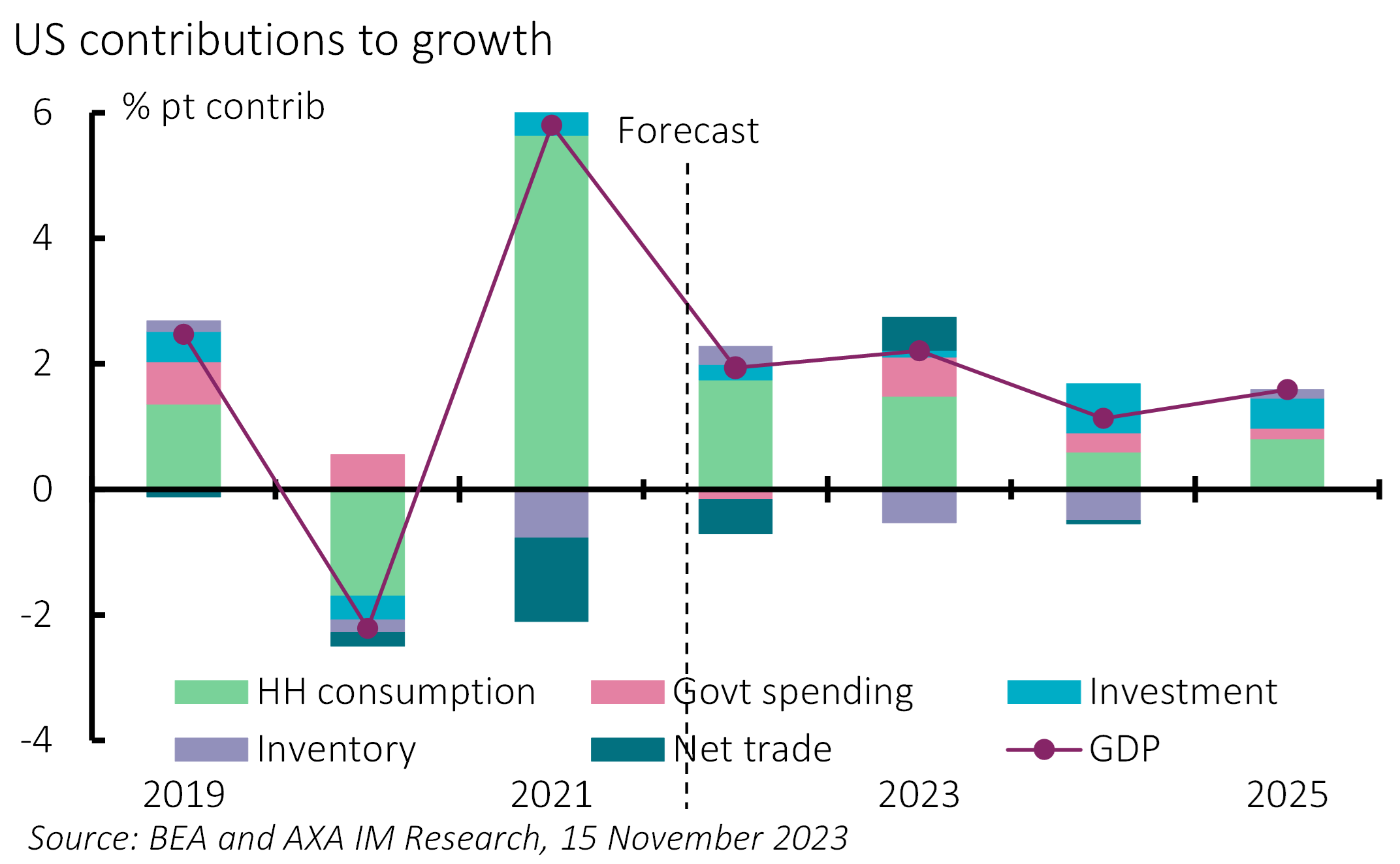

Exhibit 1: GDP on track for below-trend growth

We expect quarterly GDP growth to slow sharply in Q4 2023 (to around 1% annualised) and H1 2024, before picking up through 2025. Overall, we forecast GDP growth of 2.3% in 2023, slowing to 1.1% in 2024 and 1.6% in 2025, with quarterly growth rising above trend rates by mid-2025 (Exhibit 1). This is consistent with the Fed’s goal of a period of sub-potential growth.

Risks to our forecast are two-sided. Consumer spending could rise on increased borrowing. But we continue to suggest the balance of risks is to the downside of our outlook; a risk that our forecast of mild recession was wrong in terms of timing, not direction. Headline indicators still suggest the possibility of recession including ongoing yield curve inversion, tight credit conditions and what appears to be an impending fulfilment of the recession-indicating Sahm rule. However, we believe the aforementioned buffers have desynchronised slowdown across the economy, with a final impending softening in consumer activity anticipated. Other sectors appear now to be stabilising and could pick up, particularly in manufacturing if China’s sequential growth pace accelerates as expected.

Domestic inflation pressures

Inflation has fallen reflecting an easing in global supply chain pressures and weaker energy price rises. However, the faster-than-expected fall in headline inflation and outlook for core inflation for the coming years will depend on domestic developments – and specifically the labour market.

Despite stronger growth, labour market tightness has eased. Trend employment growth has slowed this year (to 204k in October from 334k in January), unemployment has risen (to 3.9% from 3.4%) and vacancies have fallen to 9.5mn from a peak of 12mn. This has helped wage growth slow to an annual 4.1% in October, a little over the 3.5-4% we would see as consistent with achieving the Fed’s long-term inflation mandate. Our outlook includes a further loosening of the labour market and unemployment rising to 4.4% by end-2024. However, some of this would reflect a continuation of more structural features: firmer immigration contributing to strong labour supply growth and improvement in labour matching efficiency, which should help soften wage growth, even with relatively low unemployment rates.

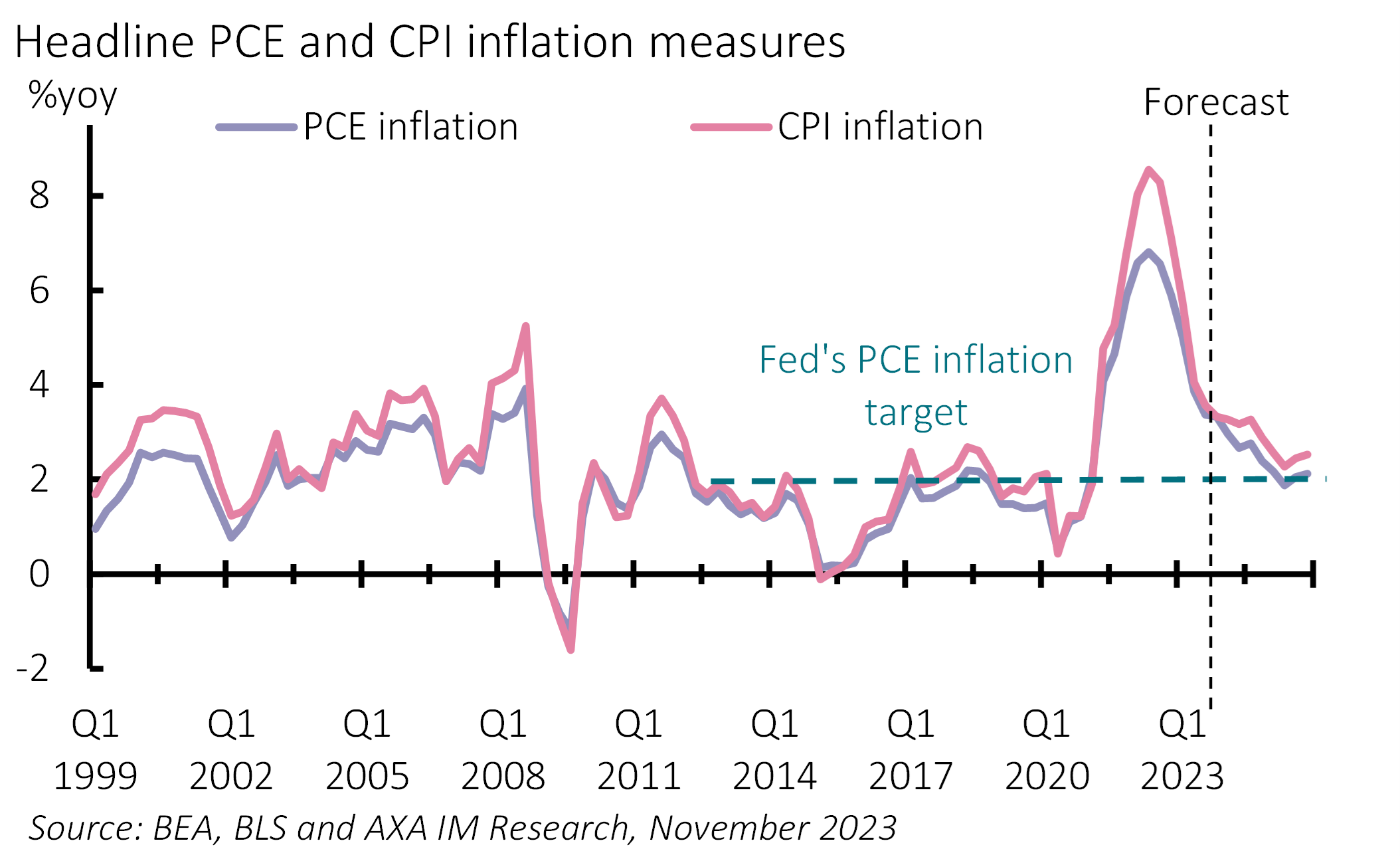

Exhibit 2: Inflation to hit target, but little room for easing

Other structural developments are likely to help reduce core inflation, including an expected fall in profit margins and a cessation of the goods and services rebalancing seen since the pandemic. On balance we forecast inflation averaging 4.2% in 2023, falling to 3.2% in 2024 and 2.7% in 2025. We forecast inflation ending 2023 at below 4%, 2024 at 2.6% and 2025 at 2.8%, with the Personal Consumption Expenditure (PCE) inflation likely falling to target in Q2 2025 (Exhibit 2).

Fed to manage restrictiveness rather than ease

We believe the Fed Funds Rate (FFR) has peaked at the current level of 5.25-50%, despite suggestions of a possible final hike. Based on our forecasts we do not see space for a significant loosening in policy over the coming two years.

Current policy is restrictive and as inflation falls, conditions will tighten further as the real FFR appreciates. Officials have discussed managing this real rate. We expect the Fed to resist reacting to economic softening but to lower the FFR to moderate real rate appreciation. We forecast 75bps of cuts from June next year, providing only a modest easing in the restrictive stance. We forecast two further cuts in 2025, taking the FFR to 4.25% by end-2025, as the Fed gently pares back restrictiveness further amid an improving growth backdrop.

We also anticipate the Fed will continue its quantitative tightening (QT) over the next two years. We think it will be comfortable reducing still “ample” reserves, with only a modest anticipated monetary tightening impact, whilst dynamically adjusting the real FFR, rather than sharply easing policy. We also expect reverse repo holdings to continue to fall over 2024. We assume that 2019 excess reserve lows act as a limit guide for future reserves (allowing for a precautionary buffer). This should see the Fed reduce excess reserves to just over $2tn, a point we estimate reaching only in early 2026. We expect it to announce ending QT only at the end of 2025. However, a sharper economic slowdown, requiring aggressive stimulus, or higher commercial bank liquidity demands risk an earlier end.

An important political year

Congress averted a government shutdown across 2023 and must now agree appropriations bills by early 2024. We forecast a modest tightening in the fiscal stance across 2024, with current plans for this to be broadly neutral in 2025. However, the US fiscal deficit is forecast at 5.9% of GDP this year and to average 5.8% for the rest of this decade, with a primary deficit of around 3%. With US debt forecast at 98% of GDP this year, US finances are sound for now but are unsustainable over the longer term and are expected to rise to 111% by 2030, 134% by 2040 and 168% by 2050. Treasury yields do not obviously price a credit premium for now (distinct from reflecting supply) and we do not forecast this. But this is a risk over the medium-term without a material fiscal tightening.

November’s Presidential Election will be key to this. It is not certain who the candidates will be, although a re-match of the 2020 Joe Biden/Donald Trump contest looks likeliest despite concerns about the former’s age and the (barely younger) latter’s legal challenges. The outcome is highly uncertain. Congressional elections will also be important. The Senate rotation looks unfavourable for Democrats, meaning a second Biden term could face a mixed or hostile Congress. A Trump win would be more likely to have a slim majority in both houses. For now, we would expect a second Trump term to focus on extending his previous tax breaks (due to expire at the end of 2025), at a further cost to the fiscal outlook. However, we would be more fearful of disruptive geopolitical developments with this outcome.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Neither MSCI nor any other party involved in or related to compiling, computing or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling, computing or creating the data have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.